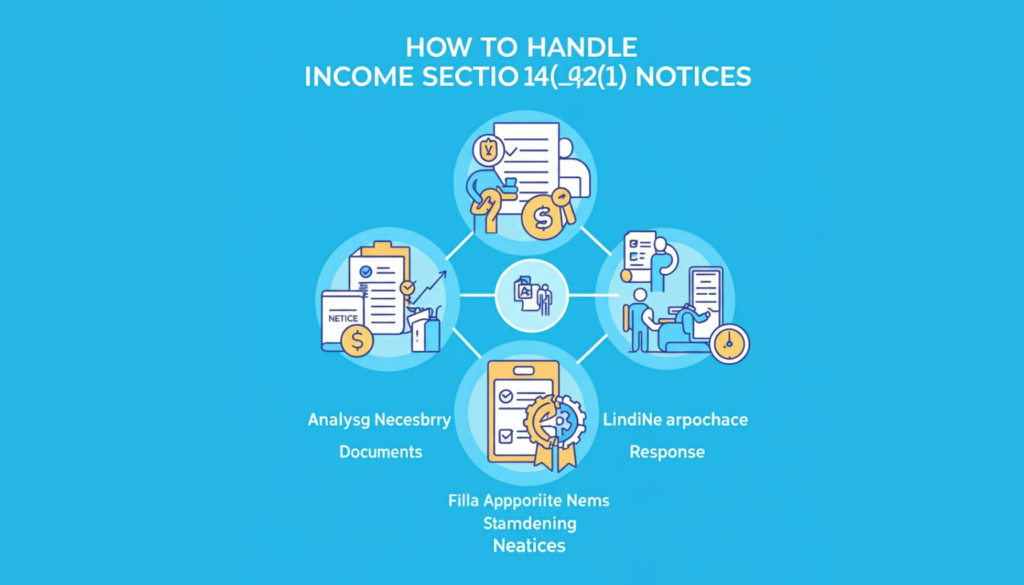

Income Tax Notice Section 142(1): Causes, Implications, and Solutions Introduction Understanding income tax notices, particularly under Section 142(1), is crucial for every taxpayer in India. This section of the Income Tax Act allows the Income Tax Department to request information, documents, or even filing of tax returns from individuals or entities. Ignoring such notices can lead to legal and financial consequences, making it essential to grasp their significance. Taxpayers often feel anxious upon receiving these notices, but with the right knowledge and timely action, the situation can be handled effectively. This blog explores Section 142(1) in detail, including its causes, implications, and actionable solutions. Whether you’re an individual taxpayer, a small business owner, or a finance professional, this guide will help you understand and manage Section 142(1) notices efficiently. Table of Contents What is Section 142(1)? Section 142(1) of the Indian Income Tax Act empowers the Income Tax Department to request specific information or documents from taxpayers. This notice is issued during the assessment process when the assessing officer requires additional details to verify a taxpayer’s income or filings. Compliance with this notice is mandatory, making it important for recipients to understand its content and act promptly. Purpose of Section 142(1) Notices The primary objective of issuing a Section 142(1) notice is to ensure compliance and collect any missing information required to assess tax liability. It can be issued for the following purposes: To file a tax return if the taxpayer has failed to do so voluntarily. To clarify inconsistencies in the taxpayer’s filings. To request additional documents or statements for assessment. Types of Notices Issued The notices under Section 142(1) generally fall into these categories: Notice for Non-Filing of Returns: Issued when a taxpayer has not filed their income tax return despite being liable to do so. Request for Additional Documentation: Seeks supplementary details like bank statements, investment proofs, or business-related documents. Clarification of Filed Data: Requires the taxpayer to explain discrepancies in information provided earlier. Type of Notice Purpose Non-Filing of Returns Request the filing of a tax return if not submitted. Additional Documentation Obtain supporting records for accurate assessment. Clarification of Filed Data Address discrepancies or mismatches in reported information. Knowing the type of notice helps in preparing an appropriate response. Causes for Receiving a Section 142(1) Notice There are several reasons why a taxpayer might receive a Section 142(1) notice. Understanding these causes allows taxpayers to avoid future issues. Non-Filing of Returns Failing to submit income tax returns within the stipulated deadlines is one of the most common triggers for this notice. This usually applies to individuals or businesses whose income exceeds the tax-free threshold but who have not filed returns. Suspicious Transactions If large deposits, high-value purchases, or unusual financial activities are flagged in your bank accounts or credit card statements, the IT department may issue a notice under Section 142(1) to investigate. Errors in Tax Filing Mistakes in tax returns, such as inconsistent or incomplete information, often prompt a notice. For instance, discrepancies between reported income and Tax Deducted at Source (TDS) records can lead to scrutiny. By identifying the root cause of the notice, taxpayers can take corrective measures more effectively. For more information read our blog :- Top 10 Income Tax Books To Stay Ahead This Tax Season Implications of Ignoring Section 142(1) Notices Ignoring a Section 142(1) notice is a risky decision. Here are the potential consequences: Penalties and Fines Failure to respond to the notice within the prescribed time can lead to financial penalties. This includes: Late filing fees: Under Section 234F, fines are imposed for delayed return submissions. Interest on Outstanding Tax: Taxpayers may accrue interest on unpaid taxes under Section 234A or 234B. Legal Consequences Non-compliance can escalate into harsher measures such as: Prosecution for tax evasion. Further scrutiny of financial records. Issuance of more stringent notices under other sections, such as Section 148. Timely action is crucial to avoid these punitive implications. How to Respond to a Section 142(1) Notice Responding to a Section 142(1) notice involves a systematic approach. Here’s a step-by-step guide: Step 1: Analyze the Notice Carefully Read the notice thoroughly to understand the nature of the request. Identify key elements such as deadlines, documents required, and the reasons for issuance. Checklist for Notice Analysis: Is the notice related to return filing, document submission, or clarification? What is the deadline for submission? Are there any specific instructions for response? Step 2: Gather Required Documents Based on the notice, compile the necessary documents. These may include: Form 16/16A for salaried individuals. TDS certificates or bank statements. Investment proofs like mutual funds, property papers, or fixed deposits. Organizing documents accurately ensures smoother submission. Step 3: File an Appropriate Response Submit the requested information through the Income Tax Department’s online portal or offline methods. Use precise and complete data while filing. Retain proof of submission for future reference. Seeking Professional Help If the notice is complex or involves large financial matters, consult a certified tax consultant or Chartered Accountant (CA). Their expertise can help avoid errors and expedite compliance. Promptly addressing the notice not only resolves the current issue but also improves credibility with the IT department. Preventive Measures for Taxpayers Prevention is always better than cure. By adopting these practices, taxpayers can minimize the chances of receiving future notices. Timely Filing of Returns Filing your income tax returns on or before the due date ensures compliance and avoids unwanted scrutiny. Accurate Documentation and Reporting Maintaining detailed financial records and reporting income accurately minimizes discrepancies. Use digital tools or consult financial experts to streamline the process. These preventive measures foster better compliance and reduce stress. Real-Life Examples or Case Studies Example 1 A salaried individual failed to file their income tax return on time due to negligence. Upon receiving a Section 142(1) notice, they promptly filed the outstanding return along with late fees and avoided further penalties. Example 2 A small business owner received a notice for mismatched TDS deductions. With the help of a CA, the business submitted accurate bank